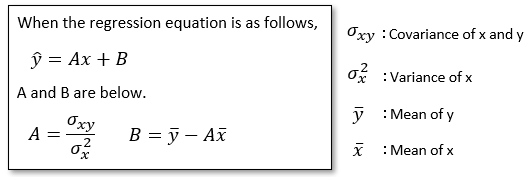

■simple regression equation by least squares method

As explained here, the formula of the simple regression equation obtained by the least squares method is as follows.

And I will explain how to derive it.

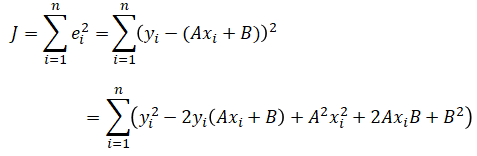

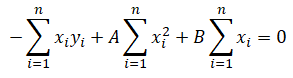

Since the least squares method finds A and B that minimize the sum of squares of the residuals from the regression equation, it is as follows.

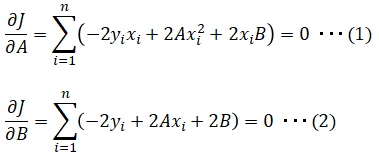

Partial differential of the above equation with A and B.

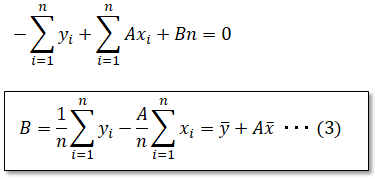

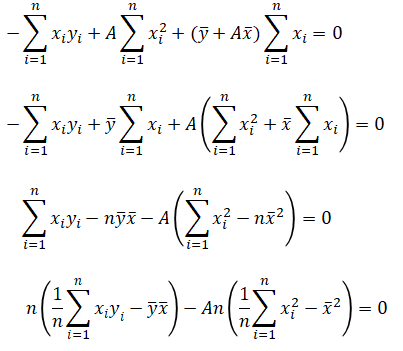

(2) is modified as follows. Each term is divided by 2 for simplicity.

Now you can find B. Dividing the sum of yi and xi by n means the average.

Next, (1) is transformed as follows. This also divides each item by 2.

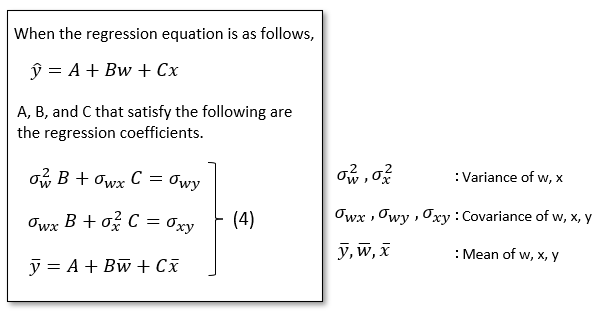

■multiple regression equation by least squares method

The formula for two variables (w, x) is as follows.

Since the concept of the derivation method is the same as for simple regression, the detailed calculation process is omitted.

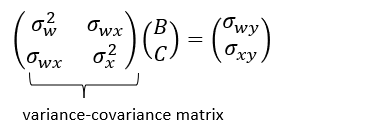

Eq. (4) can be easily understood by expressing it as a matrix as shown below, and this matrix is called a variance-covariance matrix.

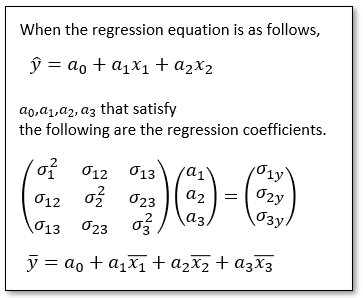

■three-variable multiple regression equation by least squares method

It will be as follows. Even if the number of variables increases, it can be handled in the same way.